[vc_row][vc_column][vc_column_text css=”.vc_custom_1646042695894{margin-bottom: 0px !important;}”]

Polyolefin producers ponder pricing policy, as feedstock costs increase.

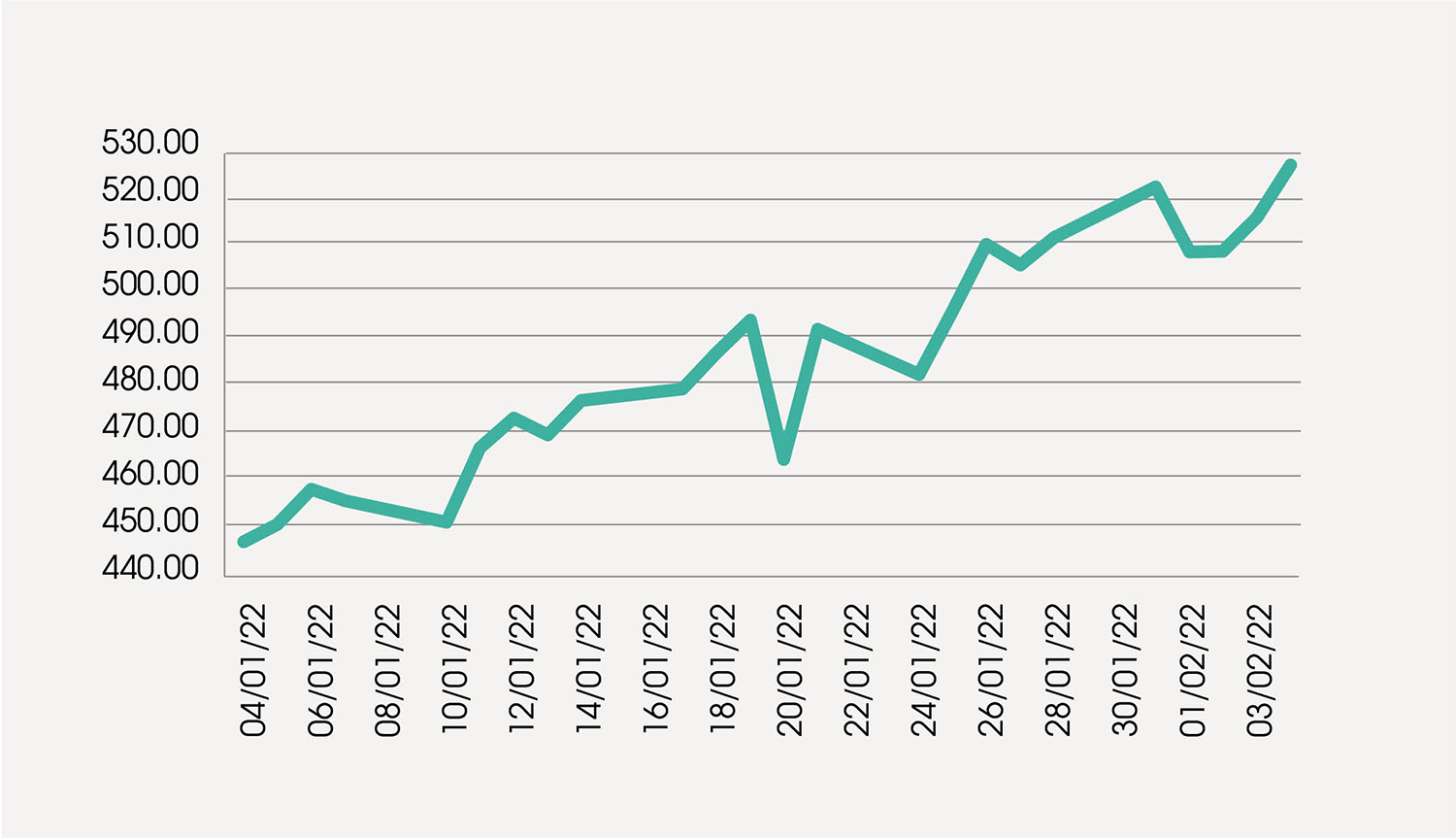

Although quite choppy due to on-going concerns about the impact of Covid-19 on the global economy, crude oil prices continue to rise. The overall recovery since April 2020 has now been more than £300 per tonne, and since concerns are diminishing regarding the likely impact of the Omicron variant the crude oil markets are increasingly bullish. Naphtha, which is a key feedstock for C2 and C3, closely tracks the price of crude oil, as illustrated above, and hence the similar increases for these feedstock references for February. However, the PP and PE markets are somewhat lacklustre, and, on this basis, there is strong resistance to the producers’ requests to pass this inflation through and it looks as if some of the margin gain that was achieved in both C2/C3 and PE/PP may have to be conceded.[/vc_column_text][mk_padding_divider][vc_column_text css=”.vc_custom_1646043093428{margin-bottom: 0px !important;}”]Brent Crude £ per tonne

[/vc_column_text][/vc_column][/vc_row][vc_row css=”.vc_custom_1637849700240{padding-top: 25px !important;}”][vc_column][vc_btn title=”Download price know-how (PDF)” style=”flat” color=”green” i_icon_fontawesome=”fa fa-arrow-down” add_icon=”true” link=”url:https%3A%2F%2Fwww.plastribution.co.uk%2Fwp-content%2Fuploads%2F2022%2F02%2Fpkh-feb-22.pdf||target:%20_blank|”][mk_padding_divider size=”20″][/vc_column][/vc_row][vc_row fullwidth=”true”][vc_column][vc_raw_html]JTVCZGZsaXAlMjBpZCUzRCUyMjY3MDUlMjIlMjAlNUQlNUIlMkZkZmxpcCU1RA==[/vc_raw_html][/vc_column][/vc_row]

[/vc_column_text][/vc_column][/vc_row][vc_row css=”.vc_custom_1637849700240{padding-top: 25px !important;}”][vc_column][vc_btn title=”Download price know-how (PDF)” style=”flat” color=”green” i_icon_fontawesome=”fa fa-arrow-down” add_icon=”true” link=”url:https%3A%2F%2Fwww.plastribution.co.uk%2Fwp-content%2Fuploads%2F2022%2F02%2Fpkh-feb-22.pdf||target:%20_blank|”][mk_padding_divider size=”20″][/vc_column][/vc_row][vc_row fullwidth=”true”][vc_column][vc_raw_html]JTVCZGZsaXAlMjBpZCUzRCUyMjY3MDUlMjIlMjAlNUQlNUIlMkZkZmxpcCU1RA==[/vc_raw_html][/vc_column][/vc_row]